Embedded Insurance vs. Captive-Backed CLIP: When Companies Should Stop Renting the Insurance Economics

- Steven Barge-Siever, Esq.

- May 2

- 6 min read

Updated: May 14

By Steven Barge-Siever, Esq.

Most companies that add insurance to their product are not building an insurance business.

They are renting one.

Quick Definitions

Embedded insurance is a distribution model where insurance is offered inside another product, platform, checkout flow, lease process, loan process, or customer journey.

A Captive CLIP is a risk-financing structure where a company uses a contractual liability insurance policy (CLIP) to support its own contractual obligations and may retain part of the underwriting economics through a captive or reinsurance arrangement.

Embedded insurance can create revenue, improve conversion, and make a product feel more complete. But in many cases, the company is still distributing someone else’s product, on someone else’s insurnace product, with someone else controlling the pricing, underwriting, claims experience, and profit.

That may be the right move for speed.

It is not the same as owning the economics.

For companies that already make warranties, guarantees, service promises, refund commitments, uptime commitments, rent protection promises, payment guarantees, or other contractual obligations, the better question is not simply:

Should we offer insurance inside our product?

The better question is:

Why are we giving away the economics of a risk we may already understand better than the market?

That is where captive-backed CLIP structures become strategically important.

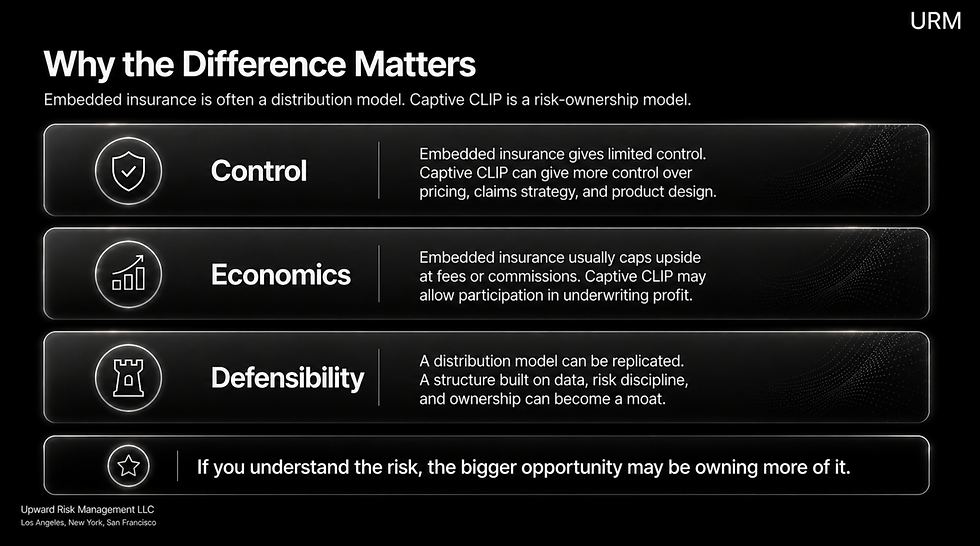

Embedded insurance is about distribution - it monetizes access to the customer.

A captive CLIP is about ownership - it monetizes control of the obligation.

Embedded Insurance: Useful, but Structurally Limited

Embedded insurance means a company offers a third-party insurance product inside its customer journey.

That may happen during checkout, onboarding, leasing, booking, financing, or subscription purchase.

It can work well.

A company can launch quickly, create ancillary revenue, improve customer convenience, and avoid taking direct underwriting risk. For many companies, that is the right first step.

But the limitation is obvious: the company may own the customer relationship, but it usually does not own the insurance economics.

The carrier, MGA, or program partner often controls the most valuable parts of the arrangement:

pricing

underwriting appetite

claims handling

policy wording

exclusions

renewal terms

long-term profitability

The platform may receive commissions, fees, or revenue share.

But the insurance engine belongs to someone else.

That creates a ceiling - Embedded insurance can monetize distribution, but it rarely gives the company full control over the risk, data, claims experience, or underwriting profit.

In plain English:

You built the storefront. Someone else owns the factory.

Captive-Backed CLIP: Owning the Obligation

A contractual liability insurance policy (CLIP) is designed to insure a company against a specific contractual obligation.

That obligation might be a warranty, service contract, refund commitment, replacement obligation, uptime credit, performance guarantee, rent default obligation, payment guarantee, or other measurable promise.

A captive-backed CLIP structure can allow a company to use licensed insurance to support that obligation while potentially retaining part of the underwriting economics through a captive or reinsurance arrangement.

The simplified structure looks like this:

The company makes a defined contractual promise.

A licensed carrier issues a CLIP to insure that obligation.

The policy reimburses the company if the covered obligation is triggered.

A captive or reinsurance vehicle assumes some of the risk behind the carrier.

The company may retain underwriting profit if the risk performs better than expected.

This is not simply adding insurance to a product.

It is converting a business obligation into a structured financial asset.

That is the strategic shift.

Why This Matters

The difference between embedded insurance and captive CLIP is not technical. It is economic.

Embedded insurance asks:

Can we offer insurance inside our product?

Captive CLIP asks:

Should we own the economics behind the promise our product already makes?

That question matters because many companies already create insurance-like risk.

A manufacturer offering an extended warranty is making a promise.

A SaaS company offering uptime credits is making a promise.

A fintech company guaranteeing payment performance is making a promise.

A proptech company supporting rent protection is making a promise.

A logistics company offering delivery guarantees is making a promise.

Once a company is making the promise, the key issue is not whether insurance can be “embedded,” it's whether the company should keep outsourcing the economics of a risk it may be uniquely positioned to understand.

If the company has credible data, predictable losses, pricing control, and operational influence over the risk, it may eventually be able to do more than distribute insurance.

It may be able to own part of the insurance value chain.

What Ownership Changes

A captive CLIP can give a company more control over:

product design

claims strategy

pricing assumptions

customer experience

underwriting data

profit retention

enterprise sales positioning

That control can become valuable.

A company that understands its own loss patterns may be able to price risk more accurately over time.

A company that controls the customer relationship may be able to manage claims more effectively.

A company that has better product data than the outside market may be able to retain profitable layers of risk instead of transferring all of it away.

Not mean every company should form a captive. But companies with scale, repeatable risk, credible data, and meaningful contractual obligations should at least ask the question. Because sometimes the most valuable insurance opportunity is not selling someone else’s policy. It's structuring your own promise.

The Regulatory Point Companies Cannot Ignore

This is where companies need to be careful. (See more Here)

There is a major difference between:

“We are selling insurance to our customers.”

and:

“We have insured our own contractual obligation.”

The first is an embedded insurance distribution model.

The second is a risk-financing structure.

That distinction can affect licensing, marketing language, policy design, consumer disclosure, claims handling, and state-by-state regulatory analysis.

A company cannot create an “insured guarantee” by adding those words to a website.

The insurance structure has to support the promise.

If the obligation is consumer-facing, warranty-like, multi-state, or marketed as insured protection, the legal and regulatory architecture must be built correctly.

The following are critical in these scenarios:

Marketing language

Policy form

Issuing carrier

Claims process

Contract wording

This is not a cosmetic distinction - it is often the difference between a scalable structure and a regulatory problem.

When Embedded Insurance Makes Sense

Embedded insurance may be the right answer when:

speed matters more than control

insurance is ancillary to the core product

the company is testing demand

the company does not have credible loss data

the company does not want underwriting exposure

an existing carrier or MGA already has a strong product

In those cases, embedded insurance can be a smart starting point.

It allows the company to test adoption, generate revenue, and learn how customers interact with the protection product.

But companies should understand what they are getting.

They are monetizing distribution.

They are not necessarily building long-term control.

When Captive-Backed CLIP Makes Sense

A captive CLIP may be worth evaluating when the:

obligation is central to the company’s value proposition

risk is measurable and repeatable

company has meaningful data

company wants underwriting profit, not only commission revenue

promise affects enterprise sales or procurement

company wants more control over claims and customer experience

company is thinking in long-term enterprise value terms

This is particularly relevant for companies with warranties, service contracts, uptime commitments, refund guarantees, payment guarantees, rent protection obligations, or other contractual promises.

Captive CLIP is not for companies casually exploring insurance.

It is for companies that understand their risk well enough to own it intelligently.

The Path to Sophistication: Start with Distribution, Move Into Ownership

The best strategy is often sequential.

A company may start with embedded insurance to test demand, collect claims data, and understand customer behavior.

Over time, it can identify profitable segments, improve pricing, negotiate better economics, participate in reinsurance, or form a captive.

Eventually, selected obligations may be supported by a CLIP structure.

That progression looks like this:

distribution revenue → data collection → underwriting insight → captive participation → CLIP-backed risk ownership

That is how a company moves from renting insurance economics to owning them.

A captive should not be built on optimism - it should be built on data.

The Bottom Line

Embedded insurance monetizes access to the customer.

Captive CLIP monetizes control of the obligation.

Embedded insurance may be the right way to start. But for companies with predictable risk, meaningful contractual promises, and credible data, it should not always be the end point.

The larger opportunity is not simply to offer insurance inside a product.

The larger opportunity is to decide whether insurance should become part of the company’s financial architecture.

For many businesses, the risk is already there.

The margin may already be there.

The data may already be there.

The question is whether the company will continue giving away the economics - or start building the structure to own them.

Connect with us:

Connect with the Author:

Steven Barge-Siever, Esq.